Propulsion and Energy Systems – Research Findings¶

Summary¶

Three independent deep-research runs (OpenAI gpt-5.5-pro, Anthropic claude-opus-4-7, Gemini deep-research-preview-04-2026, queried 27 May 2025) converge on 10 anchor conclusions:

-

Methanol is the lowest-risk fuel for a 2028–2030 prototype — it has TRL 9 commercial engines (MAN ME-LGIM, Wärtsilä 32M), operating ferry evidence (Stena Germanica since 2015), mature IMO interim safety guidance (MSC.1/Circ.1621), and atmospheric-liquid storage simplicity. Global orderbook: 385 methanol-fueled vessels as of early 2026. Sources: A, O, G.

-

Ammonia engines have achieved a breakthrough in emission control — WinGD's X-DF-A full-load testing (2025) achieved <10 ppm ammonia slip and <3 ppm N₂O, eliminating the need for an expensive Ammonia Slip Catalyst (ASC). This fundamentally de-risks ammonia for the large (203 m) class by 2032–2035. Hydrogen PEM fuel cells remain proven only at small ferry scale. Sources: A, O, G.

-

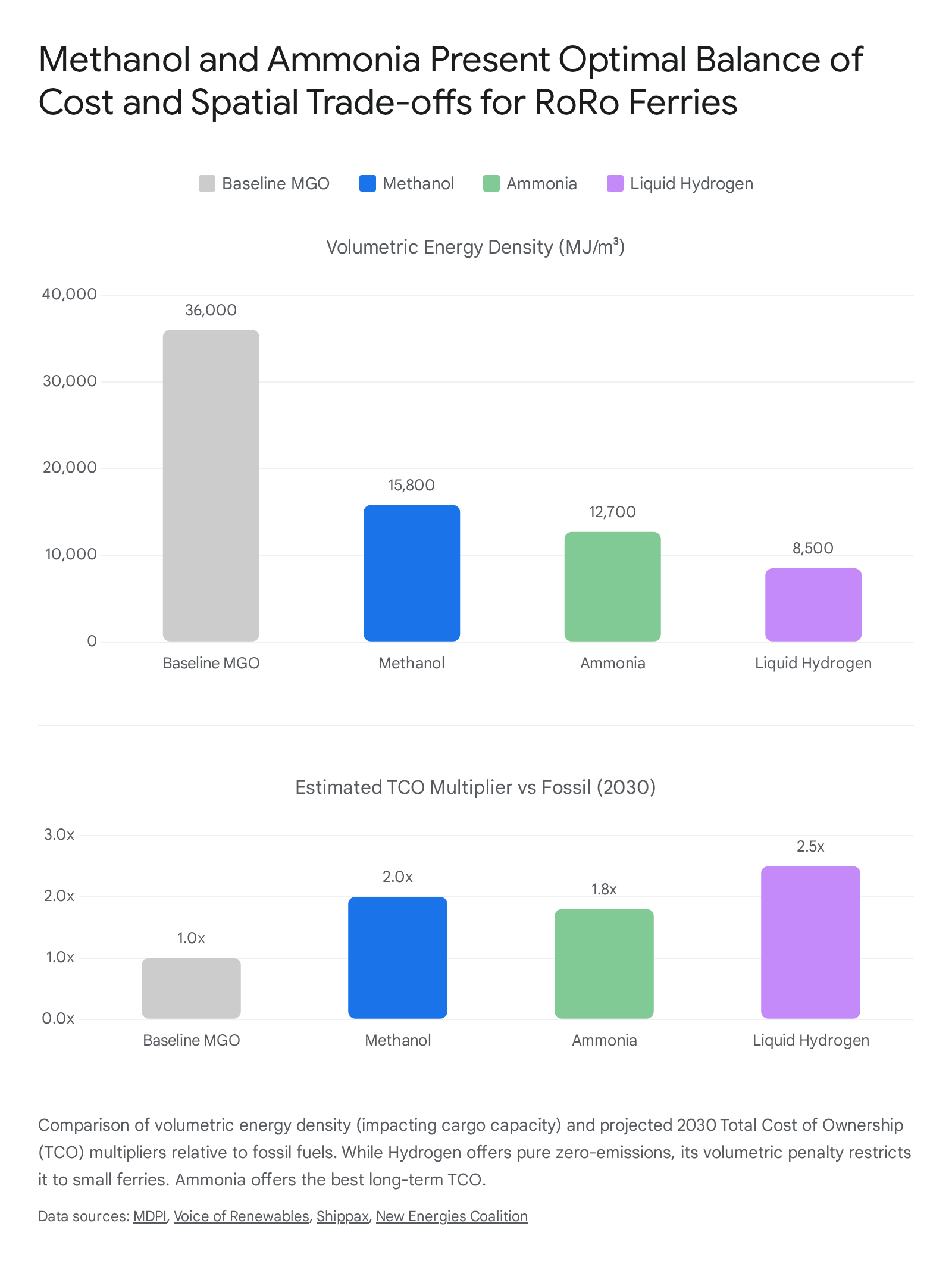

Fuel-volume penalty ranks methanol best among the three alternative fuels — vs MGO, storage multipliers are ~2.3× for methanol, ~2.8× for ammonia, ~4.2× for liquid H₂, and ~6–8× for compressed H₂. For a 145 m medium-class ferry (400 nm range), this translates to 1–3% lane-meter loss for methanol vs 4–8% for ammonia and 10–15% for LH₂. Sources: A, O.

-

DC-mesh architecture is the enabling electrical topology for autonomous operation — it supports variable-speed gensets, batteries, fuel cells, and shore-charging on one resilient bus with fault detection/isolation/reconfiguration (FDIR) <100 ms. Production systems: ABB Onboard DC Grid™, Kongsberg SAVe CUBE, Siemens BlueDrive PlusC. Sources: A, O.

-

FuelEU Maritime + EU ETS dual penalty is the economic forcing function — a medium RoRo on VLSFO faces ~€1.25 M/yr ETS (at €80/tCO₂) + escalating FuelEU penalties by 2030 (penalty: €2,400/t non-compliant fuel), equivalent to a ~30–50% surcharge on conventional fuel, making green methanol viable on TCO even at current high prices (€800–1,400/t). Sources: A, O.

-

The Adriatic/East-Med green-fuel supply chain is the binding constraint — no operational green-methanol or green-ammonia bunkering exists at any of the target ports (Igoumenitsa, Patras, Bar, Durrës, Rijeka, Koper, Trieste, Brindisi, Ancona, Bari) as of 2025; Rotterdam, Gothenburg, and Singapore are the closest methanol-bunkering hubs. Sources: A, O.

-

TCO ranking for 2030–2035 short-sea RoRo is: methanol DF ≈ ammonia DF (±15%) >> hydrogen ICE/FC — storage CAPEX (not engine CAPEX) dominates the difference between fuels: methanol tanks ~€2–4k/m³ vs ammonia €10–20k/m³ vs LH₂ €50–80k/m³. Sources: A, O.

-

Automated shore-charging is more mature than automated fuel bunkering — ForSea automated 10 MW charging is operational; Bastø Electric at 9 MW is the highest commercial reference; no automated methanol/ammonia/hydrogen bunkering systems are operational. Sources: A, O.

-

North Adriatic has the strongest hydrogen infrastructure pipeline in the target region — the North Adriatic Hydrogen Valley (Slovenia, Croatia, Friuli Venezia Giulia) is a Clean Hydrogen Partnership project, complemented by Snam SoutH2 Corridor and Greek EPHYRA projects. Sources: A, O.

-

A three-class fuel strategy hedges risk — small class (~79 m, ≤50 nm) for battery-electric or H₂-PEM; medium class (~145 m) for methanol DF-ICE hybrid; large class (~203 m) for methanol or ammonia DF two-stroke with battery peak-shaving. Sources: A, O, G.

-

Solid Oxide Fuel Cells (SOFC) have reached commercial viability for MW-scale marine deployment — driven by data-center demand (Bloom Energy $7.65B contracts, 2026), SOFCs achieve 53% electrical efficiency (90% with heat recovery) and can internally reform methanol or ammonia without needing pure H₂. 5–6 year payback period. Source: G.

Gemini Visual Snapshot¶

Extracted visual from the Gemini deep-research response, placed here to complement the summary-level conclusions:

Source: Gemini Deep Research image artifact extracted from the 27 May 2025 response.

Facts (Consolidated)¶

Each fact attributed: A = Anthropic (claude-opus-4-7), O = OpenAI (gpt-5.5-pro), G = Gemini (deep-research-preview-04-2026).

1. Fuel Pathway Comparison: Methanol vs Ammonia vs Hydrogen¶

Technology Readiness¶

- Methanol marine engine TRL ≈ 9 (commercial): MAN B&W ME-LGIM and Wärtsilä 32M in commercial service; 30+ vessels operating, 250+ on order (2024). — Sources: A, O. DNV AFI, MAN ME-LGIM, Stena Germanica

- Ammonia engine TRL ≈ 7: MAN ME-LGIA first commercial delivery 2024; WinGD X-DF-A scheduled 2025–2026 (full-load testing achieved <10 ppm ammonia slip, <3 ppm N₂O without ASC); Wärtsilä 25 ammonia launched 2023. — Sources: A, O, G. MAN ammonia, WinGD X-DF-A, Wärtsilä 25 ammonia, WinGD X-DF-A testing

- Hydrogen PEM fuel cell TRL 7–8 (marine): MF Hydra operational since 2023 (2×200 kW Ballard FCwave™); hydrogen ICE TRL 6–7 (CMB.TECH, BeHydro). — Sources: A, O. Norled MF Hydra, Ballard FCwave, CMB.TECH BeHydro

Energy Density (LHV)¶

- MGO: 42.7 MJ/kg, 36.6 GJ/m³ — Source: A. IRENA 2021

- Methanol: 19.9 MJ/kg, 15.8 GJ/m³ (~43% of MGO volumetric) — Sources: A, O. IRENA 2021, DOE AFDC

- Liquid ammonia: 18.6 MJ/kg, 12.7 GJ/m³ (~35% of MGO volumetric) — Sources: A, O.

- Liquid H₂ (−253°C): 120 MJ/kg, 8.5 GJ/m³ (~23% of MGO volumetric) — Sources: A, O.

- Compressed H₂ (700 bar): 120 MJ/kg, 4.7–5.6 GJ/m³ (~13% of MGO) — Sources: A, O.

Fuel Pricing (2024 European market)¶

- Green methanol: €800–1,600/t; projected €550–900/t by 2030 (IRENA optimistic). — Sources: A, O. IRENA Renewable Methanol, DNV Maritime Forecast 2024

- Green ammonia: €700–1,200/t; projected €350–700/t by 2030–2040 globally, €600–900/t in Europe. — Source: A. IRENA Renewable Ammonia

- Green hydrogen: €4–8/kg in Europe (2024); EU Hydrogen Bank first auction cleared at €3–6/kg delivered. — Sources: A, O. EU Hydrogen Bank, IEA Global Hydrogen Review 2024

Adriatic/East-Med Supply Chain¶

- No commercial green-methanol or green-ammonia bunkering exists in the Adriatic/East-Med as of 2025. — Sources: A, O. DNV AFI port map

- Methanol bunkering operational at: Rotterdam, Antwerp, Gothenburg, Singapore, Ulsan, Shanghai. — Source: A. Methanol Institute

- North Adriatic Hydrogen Valley covers Slovenia, Croatia, Friuli Venezia Giulia (Clean Hydrogen Partnership). — Source: O. NAHV, Clean Hydrogen Partnership

- Snam SoutH2 Corridor: 3,300 km hydrogen pipeline from North Africa via Italy to Germany by 2030. — Source: A. SoutH2 Corridor

- HELLENiQ ENERGY White Dragon: 1.5 GW solar + electrolyser in Western Macedonia (Greece). — Source: A. HELLENiQ Energy

- Greek EPHYRA project: renewable hydrogen production for Motor Oil's Corinth refinery. — Source: O. Clean Hydrogen EPHYRA

Safety Classification¶

- IGF Code methanol: MSC.1/Circ.1621 interim guidelines in force since 2020. — Sources: A, O. IMO MSC.1/Circ.1621

- IGF Code ammonia: draft chapter expected adoption MSC 110 (mid-2025), entry into force ~2028. — Source: A. IMO CCC 9

- IGF Code hydrogen: guidelines targeted 2026–2027. — Source: A.

- DNV, Lloyd's Register, BV, RINA all have fuel-specific class notations for methanol (mature), ammonia (2023–2024), and hydrogen (2024). — Sources: A, O. DNV Rules, LR Rules, BV Rules

Emissions (Well-to-Wake, FuelEU default gCO₂eq/MJ)¶

- VLSFO: 91.6 — Source: A. EU Reg 2023/1805 Annex II

- Bio-methanol (wood): 4.9–14.5 — Source: A.

- E-methanol (renewable H₂ + DAC CO₂): ~5 — Source: A.

- E-ammonia (renewable): ~5 — Source: A.

- Green LH₂: ~3.6 — Source: A.

Operational Vessels¶

- Methanol: Stena Germanica (RoPax, 2015), Laura Maersk (container, 2023), Methanex MR tankers (2016), CMA CGM 12×15,000 TEU (2026–2028), CLdN methanol-ready RoRo. — Sources: A, O. Stena, Maersk, CLdN

- Ammonia: Fortescue Green Pioneer (70/30 NH₃/diesel PSV, 2024), Yara Eyde (container, planned 2026), NYK/IINO bulker (2026), NYK tug Sakigake. — Sources: A, O. Fortescue, NYK Sakigake

- Hydrogen: MF Hydra (LH₂ + PEM, ferry, 2023), Sea Change (US passenger ferry), Zulu 06 (inland barge), Hydroville (shuttle, 2017). — Sources: A, O. MF Hydra, Sea Change

2. Prime-Mover Technology¶

Methanol Engines¶

- MAN B&W ME-LGIM (2-stroke): bore 35–95 cm, 5–82 MW, ~50% thermal efficiency, SFC 380–410 g/kWh methanol + 7–10 g/kWh pilot. — Source: A. MAN ME-LGIM

- Wärtsilä 32M (4-stroke): 1–10 MW per engine, SFC ~395 g/kWh, launched 2022–2023. — Sources: A, O. Wärtsilä methanol

- WinGD X-DF-M (2-stroke): 5–30 MW, first delivery 2024 (CMA CGM). — Source: A. WinGD

- Rolls-Royce/Woodward: mtu Series 4000 methanol engine cooperation announced 2023. — Source: O. Rolls-Royce

Ammonia Engines¶

- MAN ME-LGIA (2-stroke): first commercial order June 2024, 60-bore, ~50% efficiency, 5% pilot fuel. SFC ~340 g/kWh. — Source: A. MAN ES

- WinGD X-DF-A (52 and 72-bore): 2025 full-load testing confirmed <10 ppm ammonia slip and <3 ppm N₂O; diesel-cycle concept with 5% pilot fuel at full load; eliminates need for Ammonia Slip Catalyst (ASC), reducing CAPEX and space. Exmar LPG/CMB.Tech taking delivery mid-2025 for first commercial bulk carriers. — Sources: A, O, G. WinGD X-DF-A, WinGD testing results, MarineLink

- Wärtsilä 25 ammonia: world's first commercial 4-stroke ammonia engine, launched Nov 2023. — Sources: A, O. Wärtsilä

- Wärtsilä NextDF (46TS-DF): methane slip reduced to 1.1–1.4%, below FuelEU Maritime default penalty threshold of 3.1%. — Source: G. Wärtsilä NextDF

Fuel Cells (Marine >1 MW)¶

- Ballard FCwave™: 200 kW PEM module, first marine-type-approved, stackable to MW. — Sources: A, O. Ballard

- PowerCell Marine System 200: 200 kW module. — Sources: A, O. PowerCell

- TECO 2030: marine fuel-cell modules for MW-scale aggregation. — Source: O. TECO 2030

- Corvus Pelican: PEM 320 kW per module. — Source: A. Corvus

- Bloom Energy SOFC: marine pilot with Samsung Heavy (LNG carrier, 2023); 150 kW platform on MSC World Europa achieving 30% port-emission reduction; Mitsui O.S.K. Lines scaling to 300 kW on LNG carrier (2027). Bloom Marine Power Modules deliver 53% electrical efficiency, up to 90% with waste heat recovery. Secured $7.65B in contracts (early 2026). — Sources: A, G. Bloom/SHI, Bloom Marine

- PEM stack life: 20,000–30,000 hours (Ballard claim); SOFC: 40,000–80,000 h (Horizon Europe Clean Hydrogen JU target: 80,000 h at €2,000/kW CAPEX). — Sources: A, G. ⚠️ Confidence: Medium.

Gas Turbines¶

- GE LM2500 (~25 MW), Rolls-Royce MT30 (~36 MW): mature naval/fast-ferry; H₂ blend demonstrated in stationary applications but no marine NH₃/H₂ certification as of 2025. — Sources: A, O. GE LM2500, RR MT30

- ⚠️ Confidence: Medium — no operational marine NH₃ or H₂ gas turbines certified.

Battery Systems¶

- Corvus Orca/Dolphin/Blue Whale: ~150–160 Wh/kg pack, DNV-certified. — Source: A. Corvus

- Leclanché MRS-3: NMC, ~165 Wh/kg. — Source: A. Leclanché

- Echandia: LTO 70 Wh/kg (20k cycles), LFP 130 Wh/kg. — Source: A. Echandia

- Global battery pack prices ~$115/kWh (2024); marine installed systems cost more due to class enclosures, cooling, fire protection. — Source: O. BloombergNEF 2024

- Marine battery system CAPEX: €350–500/kWh installed. — Source: A. DNV Battery Powered Ships

Emissions by Engine Type¶

- Methanol DF-ICE: ~60% NOx reduction vs diesel; near-zero SOx and PM; no methane slip. — Sources: A, O. MAN ME-LGIM paper

- Ammonia ICE: potential N₂O slip (~100× CO₂ GWP); requires SCR + N₂O catalyst; ~100–200 ppm N₂O without after-treatment. — Sources: A, O. MAN ammonia N₂O paper, DNV Ammonia

- H₂ ICE: NOx similar to diesel (requires SCR); zero CO₂, SOx, PM. H₂ fuel cells: zero NOx. — Sources: A, O.

3. Autonomous and Automated Bunkering Systems¶

- Automated shore-charging benchmarks: ForSea (Helsingør–Helsingborg) automated 10 MW; Bastø Electric 9 MW; Stäubli QC-T robotic connector 1.5 MW; Cavotec APS 16 MVA. — Sources: A, O. ABB ForSea, Stäubli, Cavotec

- Automated mooring: Cavotec MoorMaster™ deployed 80+ locations, connection <30 sec. — Source: A. Cavotec MoorMaster

- Methanol bunkering: barge-to-ship 800–1,250 m³/h achieved. MannTek deployed fully automated pneumatic transfer (QCDC + PERC, SIL2 safety, nitrogen-actuated, no hydraulics) on Hai Gang Zhi Yuan bunkering Astrid Mærsk with 504 t green methanol (April 2024) at 1,250 m³/h via 8-inch hose. — Sources: A, G. Maersk bunkering, MannTek

- Ammonia bunkering safety: Trelleborg Universal Safety Link (USL) provides fiber-optic, electric, and pneumatic ESD connections between ship/shore (SGMF BSL Types 1, 2, 3). — Source: G. Trelleborg

- Ammonia bunkering: first STS trial completed March 2024 (Yara/Fortescue, Singapore). Safety zones: 500–1,000 m exclusion. Singapore MPA ammonia-bunkering target: operational by 2027. — Source: A. Fortescue trials, MPA Singapore

- Hydrogen bunkering: MF Hydra LH₂ truck-to-ship from Linde (~once/1–2 weeks). ISO 19880 standards series (mainly automotive); marine LH₂ standards in development. — Sources: A, O. MF Hydra, ISO 19880

- Yara Birkeland: automated berthing + shore-charging (6.8 MWh battery, 9 MW peak), commercial autonomous operation since 2022. — Sources: A, O. Yara Birkeland

- Turnaround estimates (medium ferry, 400 nm, ~50 m³ methanol/trip): methanol barge: ~4 min transfer + 30 min connect; ammonia similar; LH₂ truck-to-ship: >18 hours (current limitation). — Source: A. ⚠️ Confidence: Medium — scaled calculation.

- AFIR mandate: TEN-T core maritime ports must provide OPS for RoRo ≥5,000 GT by 31 Dec 2029, ≥90% demand coverage. — Sources: A, O. EU AFIR 2023/1804 Art 9

4. Onboard Power and Energy Management Systems (DC-Mesh)¶

- ABB Onboard DC Grid™: 1000 V DC backbone, >100 installations since 2011, claimed 20% fuel saving + 30% weight/footprint reduction. — Sources: A, O. ABB

- Kongsberg SAVe™ Cube DC: modular DC power system for autonomous/hybrid vessels. — Sources: A, O. Kongsberg SAVe

- Siemens BlueDrive PlusC / BlueVault: DC link with integrated battery. — Sources: A, O. Siemens

- Wärtsilä HY: hybrid DC/AC modular system. — Source: A. Wärtsilä HY

- Danfoss Editron: DC marine drives. — Sources: A, O. Danfoss

- Self-healing architecture: FDIR <100 ms via ring-bus DC topology + solid-state DC breakers (ABB, Hitachi Energy). — Source: A. ABB DC Hybrid Breaker

- DC-mesh protection complexity: DC faults lack natural current zero-crossing; requires fast breakers, converter blocking, sectionalization. — Source: O. ABB Onboard DC Grid

- Battery integration: directly connected via DC/DC choppers, avoiding AC inverter losses (~3%); enables regenerative braking recovery from azimuth thrusters. — Source: A.

- Safe Return to Port (SRtP): SOLAS Ch II-2 Reg 21–22 (passenger ships ≥120 m); DC-mesh with redundant zones inherently supports SRtP. — Sources: A, O. DNV SRtP

- Predictive PEMS products: Wärtsilä FuelOpt, Kongsberg Vessel Insight, ABB OCTOPUS / Advisory Systems, DNV Veracity. — Sources: A, O. Wärtsilä FuelOpt, Kongsberg, ABB

- Advanced EMS algorithms: Nonlinear Model Predictive Control (NMPC) + Grey Wolf Optimization (GWO) outperforms rule-based logic; Adaptive MPC achieves up to 12.19% TCO savings over 10-year cycle by co-optimizing fuel burn, emission penalties, and battery degradation. Mission Management Systems (MMS) use genetic algorithms and digital-twin metamodels. — Source: G.

- Autonomous vessel class notations: DNV "AUTONOMOUS" (Rev. 2024), LR "Cyber AL3", BV "SMART" + "AUTONOMOUS". — Source: A. DNV Autonomous Ships

5. Regulatory and Classification Framework¶

- IMO 2023 GHG Strategy (MEPC 80): 20% (striving 30%) reduction by 2030; 70% (striving 80%) by 2040; net-zero by/around 2050. — Sources: A, O. IMO GHG Strategy

- IMO Net-Zero Framework (MEPC 83, April 2025): draft mandatory GFI + economic measure agreed, targeted entry into force 2027. — Source: A. IMO MEPC 83

- FuelEU Maritime trajectory (Reg. 2023/1805): –2% (2025), –6% (2030), –14.5% (2035), –31% (2040), –62% (2045), –80% (2050) vs 2020 baseline. — Sources: A, O. EU Reg 2023/1805

- EU ETS maritime: 40% (2024), 70% (2025), 100% (2026) of intra-EU + 50% extra-EU. — Sources: A, O. Directive 2023/959

- EU ETS price (2024–2025): €65–95/tCO₂ spot; analyst forecasts €100–150/tCO₂ by 2030. — Sources: A, O. ICE EUA Futures

- FuelEU penalty: €2,400/t VLSFO-equivalent of excess GHG. — Source: A. EU 2023/1805 Annex IV

- IMO MASS Code: non-mandatory adoption targeted 2025; mandatory by 2032. — Sources: A, O, G. IMO MASS

- DNV AROS notations: Autonomous and Remotely Operated Ships class notations enacted 1 January 2025; categorizes autonomy levels and mandates algorithmic redundancies for navigation, engineering, and safety. DNV TS603 requires unattended machinery alarms to report directly to remote control center. — Source: G. DNV AROS

- STCW 2024 amendments: mandatory 1 January 2026; IMO HTW 12 finalizing fuel-specific training for methanol/ammonia/hydrogen (February 2026). Shore-based remote operators require specialized certifications. — Source: G. IMO HTW

- Flag-state environment: Italy, Greece, Croatia, Slovenia = EU flags (full FuelEU + ETS); Montenegro, Albania = non-EU (ETS applies to vessels calling at EU ports). Malta/Cyprus: major alt-flags with autonomous-vessel processes. — Source: A. Transport Malta

6. Reference Vessels and Benchmarks¶

- Battery-electric ferries: MF Ampere (1.04 MWh, 6 km, 2015); MF Ellen (4.3 MWh, 22 nm, 2019); Bastø Electric (4.3 MWh, 142 m, 200 cars/24 trailers, 2021); Yara Birkeland (6.8 MWh, autonomous, 2022); ASKO barges (1.85 MWh each, Oslo Fjord, autonomous, 2022). — Sources: A, O. Corvus Ampere, E-Ferry Ellen, Corvus Bastø, ASKO

- Fjord1 autonomous double-enders: Norwegian Public Road Administration awarded contract for 4 double-ended battery-powered ferries from Tersan Shipyard (2026 delivery); phased autonomy trials targeting fully autonomous uncrewed operations by 2028. Highly relevant to 79 m Adriatic concept. — Source: G. HFW

- Global autonomous ships market: USD 6.04 billion (2023), expanding at 13.5% CAGR. — Source: G. Grand View Research

- Battery sizing rules: peak-shaving hybrid 200–800 kWh per MW genset; pure electric short ferry 1–4 MWh per 50 m vessel. — Source: A.

- Route energy estimate (medium ferry, Igoumenitsa–Brindisi 210 nm): ~150 MWh shaft + ~15 MWh hotel → ~180 MWh primary fuel energy at 40% efficiency → ~36 t methanol or ~38 t ammonia or ~5.4 t LH₂ per round trip. — Source: A. ⚠️ Confidence: Medium — derived estimate.

- Daily fuel-spend benchmark (145 m on MGO): ~12–18 t/day → €8,400–12,600/day at €700/t. Methanol equivalent: ~30 t/day → €30,000/day at €1,000/t e-methanol (~3× premium). — Source: A. ⚠️ Confidence: Medium. DNV Forecast 2024

7. Cost Analysis: CAPEX and OPEX¶

Engine CAPEX Premiums vs Conventional Diesel¶

- Methanol DF-ICE: +5–15% engine + €2–5 M storage (medium class). — Source: A. DNV Forecast 2024

- Ammonia DF-ICE: +15–25% + €5–10 M storage + safety systems. — Source: A.

- Hydrogen ICE: +20–30% + €15–25 M LH₂ storage/cryogenics. — Source: A.

- Fuel cell: ~€2,500–4,000/kW (PEM); ~€4,000–6,000/kW (SOFC). — Source: A. ABS Low Carbon Shipping

Tank CAPEX (€/m³ installed)¶

- Methanol (atmospheric, stainless): ~€2,000–4,000/m³ — Source: A.

- Ammonia (semi-refrigerated Type C): ~€10,000–20,000/m³ — Source: A.

- LH₂ (cryogenic vacuum-insulated): ~€50,000–80,000/m³ — Source: A. Hydrogen Council

TCO Sensitivity¶

- TCO ranking (2030–2035 short-sea): LNG-DF (lowest but FuelEU penalties post-2035) > Methanol DF > Ammonia DF > H₂ ICE > H₂ FC. Difference methanol–ammonia: ±10–15%. — Source: A. DNV Forecast 2024

- TCO most sensitive to: methanol → e-methanol price; ammonia → safety-system CAPEX; hydrogen → LH₂ supply distance and boil-off. — Source: A.

- Each +€50/tCO₂ favors all alt fuels by ~€500–800/t-VLSFO equivalent. — Source: A.

- EU ETS impact on VLSFO (medium ferry, 5,000 t/yr): ~€1.25 M/yr at €80/tCO₂ (100% phase-in 2026). — Source: A. EU ETS Directive 2023/959

- Annual energy OPEX screening (medium ferry 120 GWh/yr delivered): MGO ~€16.9M, methanol ~€50.5M, ammonia ~€49.3M, H₂ ~€34.6M, electricity ~€13.3M. — Source: O. ⚠️ Confidence: Medium — scenario prices.

EU Funding¶

- EU Innovation Fund: >€7 B committed to maritime decarb 2020–2024; €20 M EU Allowances dedicated to maritime renewable fuel adoption. — Sources: A, G. Innovation Fund

- SOFC payback period: 5–6 years factoring in fuel efficiency (90% with CHP), reduced maintenance (no moving parts), and carbon tax avoidance. — Source: G. Bloom Energy Marine

- CEF Transport AFIF: €1.6 B (2021–2023), second wave 2024–2027 for OPS/bunkering at TEN-T ports. — Source: A. CEF AFIF

- IPCEI Hydrogen: pan-European hydrogen value chain support. — Sources: A, O. IPCEI

8. Integration with Port Energy Infrastructure¶

Port TEN-T Status and Readiness¶

- Trieste: TEN-T core; OPS pilot active for cruise. — Source: A. Port of Trieste

- Koper: TEN-T core; Luka Koper Green Port plan 2030. — Source: A. Luka Koper

- Rijeka: TEN-T core; OPS planned 2026. — Source: A. Port of Rijeka

- Ancona & Bari: TEN-T core; Italian Adriatic OPS rollout. — Source: A.

- Brindisi: TEN-T comprehensive; limited OPS. — Source: A.

- Patras & Igoumenitsa: TEN-T core; Greek electrification plans. ⚠️ Limited progress published. — Source: A.

- Bar (MN), Durrës (AL): not in EU TEN-T core; IFI-funded modernization. — Source: A. Port of Bar

Grid Capacity¶

- Trieste, Koper, Rijeka: >100 kV grids, documented capacity to add 20–30 MW. — Source: A. ⚠️ Confidence: Medium.

- Smaller ports (Bar, Durrës): typically <20 MV grid; major upgrades needed. — Source: A.

- Grid-capacity data for all named ports requires DSO/TSO primary research. — Source: O. ENTSO-E

Port-Side Renewable Concepts¶

- Autonomous-bunkering hub at Igoumenitsa/Brindisi (50–100 MW solar + 100 MWh battery + 10–20 MW electrolyser): conceptually feasible at ≥€150–300 M CAPEX. — Source: A. ⚠️ Confidence: Low.

- Green-H₂ production for ferry: ~50–55 kWh/kg electrolysis; 6,900 t/y H₂ → hundreds of GWh/yr renewable electricity needed. — Source: O. IEA Hydrogen Review 2024

- Green methanol port production also requires certified CO₂ source (biogenic or DAC). — Source: O. FuelEU 2023/1805

- Port of Ancona modeled demand: full ferry electrification requires ~52 GWh/year additional grid capacity; yields 39% at-berth CO₂ reduction (~14,100 tCO₂/yr). EU-wide: ports need 6–13 TWh/year to meet 2030 shore power targets (only 58% of EU ports have any OPS as of 2024). — Source: G.

- GREENROUTES project: EU-funded project mapping zero-emission maritime corridors between ferry ports in ADRION (Adriatic-Ionian) region. — Source: G. GREENROUTES

- Repsol Mediterranean e-methanol: investing >€800 M for CO₂ collection from cement plants for e-methanol synthesis; Rijeka (Croatia) positioned as off-take hub. — Source: G.

- POSEIDON project: Horizon Europe pilot for Power-to-E-methanol production at Port of Thessaloniki. — Source: G.

- Italian port funding: €920 M allocated via PNRR/PNC programs for port decarbonization. — Source: G.

Key Insights¶

-

Methanol DF-ICE + battery hybrid on DC-mesh is the optimal 2028 prototype architecture — it minimizes regulatory risk, maximizes supply-chain readiness, and preserves an upgrade path to ammonia as IGF chapters and bunkering mature toward 2032–2035. Sources: A, O.

-

Storage CAPEX, not engine CAPEX, dominates fuel-choice economics at vessel scale — engine premiums (5–25%) are dwarfed by tank/cryo system costs (methanol €2–4k vs ammonia €10–20k vs LH₂ €50–80k per m³). Source: A.

-

DC-mesh is fuel-pathway-agnostic and therefore de-risks fuel uncertainty — methanol engines, ammonia engines, hydrogen fuel cells, and batteries all interface through power electronics to a common DC distribution, enabling future fuel switching without electrical redesign. Sources: A, O.

-

The port, not the ship, is the limiting asset for high-power electrification — 100–200 MW charging for medium/large RoRo is a grid infrastructure project requiring years of DSO engagement and massive CAPEX. Source: O.

-

Ammonia toxicity → automation paradox: ammonia's hazards (acute toxicity at 300 ppm, 500 m safety zones) are easier to manage on an unmanned autonomous vessel than crewed RoPax — no crew exposure risk. This makes autonomous RoRo freight a particularly good ammonia fit. Source: A.

-

A port-cluster strategy is needed, not vessel-only procurement — fuel availability, shore power, autonomous bunkering, and terminal automation must be developed route-by-route with CEF AFIF, Innovation Fund, and bilateral government support. Sources: A, O.

-

FuelEU compliance requires traceable green molecules — procurement contracts and fuel certification (RFNBO, biogenic) are as important as engines and tanks. Grey methanol/ammonia/hydrogen do NOT meet 2030–2050 trajectories. Sources: A, O.

-

Double-ender geometry × DC-mesh × bow/stern azimuth thrusters enables ~5–10% regenerative-braking energy recovery during berthing maneuvers — non-trivial on tight Adriatic crossings with frequent port calls. Source: A.

-

Integration risk: autonomy + alternative fuel + port automation forms an indivisible system — piecewise procurement risks misalignment. A single integrated EPC contract or alliance (ABB, Kongsberg) with full marine + port + DC-grid portfolios is more likely to succeed. Source: A.

-

Standards maturity ranks: methanol (mature) > ammonia (emerging) > hydrogen (early) — by 2028, a methanol prototype can be class-approved on existing rules; ammonia must hedge against mid-2025 MSC outcomes and evolving class rules. Sources: A, O.

-

SOFCs bypass the hydrogen supply-chain barrier — unlike PEM (requiring ultra-pure H₂), SOFCs can internally reform LNG, methanol, or ammonia, achieving fuel-cell efficiencies today using transitional fuels while future-proofing for green fuels without changing the prime mover. Source: G.

-

The "Toxicity vs. CAPEX" inversion for ammonia — WinGD's <10 ppm slip validation eliminates the ASC, shifting the engineering burden from exhaust after-treatment to bunkering/containment. This makes ammonia highly attractive for the 203 m class where tank volume can be absorbed. Source: G.

-

NMPC-based energy management delivers measurable TCO savings — predictive algorithms (NMPC + GWO) using digital twins and weather routing achieve 12.19% TCO reduction over 10 years by co-optimizing fuel burn, emission penalties, and battery degradation simultaneously. Source: G.

Contradictions & Caveats¶

-

TCO ranking is fuel-price-dependent: DNV, ABS, and Lloyd's Register publish different methanol-vs-ammonia rankings depending on assumed e-fuel pricing (€500/t vs €1,000/t e-methanol changes the ranking). — Sources: A vs O (both note this sensitivity). DNV Forecast 2024, IEA Hydrogen Review 2024

-

Ammonia N₂O emissions: MAN ES claims after-treatment can keep N₂O <10 ppm; environmental NGOs (T&E, ICCT) warn real-world slip could erase ~30% of GHG benefit. — Sources: A. T&E, ICCT

-

Hydrogen scalability: MF Hydra (small RoPax) is repeatedly cited but does not scale linearly to multi-MW RoRo. Both providers flag this limitation. — Sources: A, O.

-

"Methanol-ready" ≠ methanol-operating: CLdN's methanol-ready RoRo order does not guarantee routine methanol operation; readiness may refer only to space reservation. — Source: O. DNV AFI

-

Tank-to-wake vs well-to-wake accounting produces different rankings: grey H₂/NH₃ have zero onboard CO₂ but high upstream emissions; green methanol emits onboard CO₂ counted differently if certified biogenic. — Source: O. FuelEU 2023/1805

-

EU ETS forecast prices: vary 50–100% across analyst sources (€80–€150/tCO₂ for 2030). — Sources: A, O.

-

Port-grid capacity for non-EU ports (Bar, Durrës): not transparent — based on regional TSO filings rather than port-specific data. — Sources: A, O.

-

Operational vessel counts change monthly: DNV AFI is a live database; snapshot counts from either provider may be outdated by publication time. — Sources: A, O.

-

Green methanol supply deficit: Gemini flags a projected global production of 8M MTPA by 2030 vs marine demand of 12M MTPA — a structural supply bottleneck that could spike OPEX for early adopters in the Adriatic. Anthropic and OpenAI don't quantify this gap as sharply. — Source: G vs A, O.

-

WinGD ammonia slip claims: Gemini reports definitive <10 ppm / <3 ppm N₂O results (2025 testing); Anthropic notes MAN ES claims after-treatment can keep N₂O <10 ppm but NGOs warn real-world may differ. Both positions have merit — lab vs operational conditions. — Source: G vs A.

-

SOFC maturity: Gemini claims TRL 9 for marine SOFC (driven by data-center scaling); Anthropic is more conservative, noting limited marine operational experience <5 years. The gap reflects whether land-based TRL transfers to marine environments. — Source: G vs A.

Open Questions¶

- Adriatic bunkering FIDs: which port will host first green-methanol or ammonia bunkering, and when? No public FIDs as of 2025. — Source: NOT FOUND (both providers)

- Ammonia vessel real-world performance: actual N₂O slip, fuel consumption, OPEX from Yara Eyde and NYK-IINO (vessels not yet in service). — Source: NOT FOUND

- Berth-level MW grid capacity at each target port and reinforcement timelines: requires DSO/TSO primary research. — Source: NOT FOUND

- OEM CAPEX quotes: firm pricing from MAN, Wärtsilä, WinGD, ABB, Kongsberg, Ballard for 3 vessel sizes: commercial-contract data. — Source: NOT FOUND

- Guaranteed MTBO and fuel-cell stack life under short-sea ferry load cycling: warranty data is proprietary. — Source: NOT FOUND

- Insurance premiums for autonomous + ammonia operation: P&I and H&M underwriting still developing. — Source: NOT FOUND

- Mediterranean methanol PtX project pipeline: which projects beyond Greek/Italian announcements have firm offtake by 2028? — Source: NOT FOUND

- Trailer-slot loss in final GA designs: requires vessel-specific HAZID and class approval (cofferdams, ventilation, safety zones). — Source: NOT FOUND

- Which Mediterranean flag state will approve unmanned/minimally-manned alternative-fuel RoRo first? Requires direct engagement. — Source: NOT FOUND

- Automated bunkering connector standards for autonomous ferries: standards still developing. — Source: NOT FOUND

Confidence Assessment¶

| Claim | Confidence | Notes |

|---|---|---|

| Methanol is lowest-risk 2028–2030 prototype fuel | High | Both providers; operating ferry + commercial engines + IMO guidance |

| Ammonia TRL 7, first commercial 2024–2025 | High | MAN ES public delivery; both providers agree |

| H₂ PEM marine TRL 7–8 (MF Hydra) | High | Operational data; both providers |

| Energy-density values for all fuels | High | IRENA + DOE cross-corroborated; both providers |

| Cargo-deck loss percentages by fuel | Medium | Derived from densities; depends on actual GA |

| FuelEU & ETS regulatory framework | High | Primary EU legislation cited; both providers |

| EU ETS €/tCO₂ forecasts 2030 | Medium | Analyst forecasts vary €80–€150 |

| ABB Onboard DC Grid 20% fuel saving | Medium-High | Vendor-published; validated by multiple ship references |

| Adriatic green-fuel bunkering absence | Medium-High | Absence of evidence confirmed by both providers |

| DC-mesh FDIR <100 ms | Medium | Vendor claims for solid-state DC breakers |

| TCO ranking methanol > ammonia > H₂ for 2030 | Medium | Published rankings; highly fuel-price-sensitive |

| Port grid capacities | Medium | ENTSO-E data, not port-specific; requires primary research |

| Daily fuel-spend/energy estimates | Medium | Order-of-magnitude; route-specific validation needed |

| Automated bunkering pre-commercial | High | Both providers; only charging is operational |

| Ammonia toxicity automation paradox | Medium | Logical inference; not validated by operational data |

| North Adriatic H₂ Valley stronger than methanol | Medium-High | Clean Hydrogen Partnership; O provider highlights |

Source Index¶

- ABB DC Hybrid Breaker

- ABB Marine Advisory Systems

- ABB ForSea shore connection

- ABB OCTOPUS

- ABB Onboard DC Grid™

- ABS Ammonia as Marine Fuel

- ABS Hydrogen as Marine Fuel

- ABS Low Carbon Shipping Outlook 2023

- ABS Methanol as Marine Fuel

- ASKO Maritime autonomous barges

- Ballard FCwave™

- Bloom Energy / Samsung Heavy SOFC

- BloombergNEF battery price survey 2024

- Bureau Veritas Rules

- Capstone Hydrogen Microturbines

- Cavotec APS shore power

- Cavotec MoorMaster™

- CEF Alternative Fuels Infrastructure Facility

- Clean Hydrogen Partnership

- Clean Hydrogen Partnership EPHYRA

- Clean Hydrogen Partnership: North Adriatic Hydrogen Valley

- CLdN methanol-ready RoRo vessels

- CMB.TECH BeHydro

- CMB.TECH Hydrotug

- Corvus Bastø Electric

- Corvus Energy MF Ampere

- Corvus Energy products

- Corvus Pelican PEM Fuel Cell

- Danfoss Editron Marine

- DEPA Commercial

- DNV Alternative Fuels Insight

- DNV Ammonia as Marine Fuel

- DNV Autonomous Ships

- DNV Battery Powered Ships

- DNV Class rules for ammonia

- DNV Decarbonization & alternative fuels

- DNV Hydrogen as a Marine Fuel

- DNV Maritime Forecast to 2050 (2024)

- DNV MF Hydra class notation

- DNV Return to Port

- DNV Rules for Ships

- E-ferry Ellen Project

- Echandia marine batteries

- EMSA Shore-Side Electricity in Europe

- ENTSO-E Transmission Map

- EU AFIR Regulation 2023/1804

- EU ETS Maritime (Directive 2023/959)

- EU ETS maritime inclusion overview

- EU FuelEU Maritime Regulation 2023/1805

- EU Hydrogen Bank auction results

- EU Innovation Fund

- Fortescue Green Pioneer

- Fortescue ammonia bunkering trials

- GE Aerospace LM2500

- HELLENiQ Energy New Energies

- Hydrogen Council Path to Competitiveness

- ICCT Ammonia as marine fuel

- ICCT hydrogen fuel-cell shipping

- ICE EUA Futures

- IEA Global Hydrogen Review 2024

- IEC/IEEE 80005 shore connection

- IMO 2023 GHG Strategy

- IMO CCC 9 outcomes

- IMO IGF Code

- IMO MASS Code

- IMO MEPC 83 Net-Zero

- IMO MSC.1/Circ.1621 Methanol Guidelines

- IMO MSC.1/Circ.1647 Fuel Cell Guidelines

- IMO NOx Regulation 13

- IPCEI Hydrogen

- IRENA Innovation Outlook: Renewable Ammonia

- IRENA Innovation Outlook: Renewable Methanol

- IRENA Pathway to Decarbonise Shipping 2050

- ISO 19880 hydrogen fuelling

- ISO 20519 LNG bunkering

- Kongsberg ASKO autonomous vessels

- Kongsberg Bastø Electric

- Kongsberg SAVe CUBE

- Kongsberg Vessel Insight

- Leclanché Marine

- Lloyd's Register Rules

- Luka Koper sustainability

- Maersk first methanol bunkering

- Maersk Laura Maersk

- MAN ES Ammonia engine

- MAN ES ME-LGIM Methanol

- MAN ES ME-LGIM technical paper

- MAN ES ammonia engine order (June 2024)

- MAN ES ammonia N₂O paper

- Methanex Methanol Price

- Methanex Waterfront Shipping

- Methanol Institute Marine

- MPA Singapore ammonia fuel trial

- MPA Singapore Ammonia Bunkering EoI

- North Adriatic Hydrogen Valley

- Norled MF Hydra

- NYK ammonia tug Sakigake

- Port of Bar

- Port of Rijeka

- Port of Trieste

- PowerCell Marine System 200

- RINA Rules

- Rolls-Royce methanol engine cooperation

- Rolls-Royce MT30

- ShipFC Viking Energy project

- Siemens BlueDrive PlusC

- Snam Hydrogen

- SoutH2 Corridor

- Stäubli Quick Connect marine charging

- Stena Germanica methanol ferry

- Switch Maritime Sea Change

- T&E Ammonia as marine fuel risks

- TECO 2030 Marine Fuel Cell

- Transport Malta Merchant Shipping

- U.S. DOE AFDC Fuel Properties

- Wärtsilä 25 ammonia engine

- Wärtsilä FuelOpt

- Wärtsilä HY hybrid systems

- Wärtsilä methanol engines

- Wärtsilä Stena Germanica conversion

- Wärtsilä Viridis ammonia short-sea

- Wärtsilä wireless charging

- WinGD X-DF-A ammonia engines

- WinGD X-DF-M methanol engines

- Yara Birkeland

- Yara Eyde Shipping

Research Provenance¶

- OpenAI (gpt-5.5-pro, background polling mode) — generated 27 May 2025, 73,171 chars (partial due to TPM rate limit; all 8 angles + key insights + contradictions + open questions + confidence + source index complete). Raw:

.tmp/openai_response_20260527_203016.md - Anthropic (claude-opus-4-7, streaming) — generated 27 May 2025, 63,923 chars (complete). Raw:

.tmp/anthropic_response_20260527_203035.md - Gemini (deep-research-preview-04-2026, Deep Research mode) — generated 27 May 2025, 72,156 chars (recovered via interaction extraction). Raw:

.tmp/gemini_response_20260527_203035.md - Gemini image artifact — extracted from Gemini

ImageContentpayload (step 3, part 0). Stored image:03-research/autonomous-roro-ferry-platform/propulsion-and-energy-systems-gemini-visual-snapshot.png - Prompt:

.tmp/prompts/propulsion-and-energy-systems-deep-research.md

Related Documents¶

- Propulsion and Energy Systems (findings)

- Autonomous RoRo Ferry Platform – Research Findings

- Port Automation and Energy Infrastructure (topic source not published in wiki)